If you are dealing with a rental property shortfall in Canada, you are not alone. Hundreds of landlords across the GTA and beyond are covering a $400- $500 gap every month, and most are doing so in the most expensive way possible.

The Rental Property Shortfall Canada Landlords Ignore

Most landlords write a cheque from their chequing account every month. Clean, simple, no new debt. It feels responsible. But here is the problem: that money came from your paycheque. Which means before it hit your account, CRA already took its share. You earned significantly more gross than you needed to net that amount.

The tax code gives you a legitimate way to subsidize that shortfall — most landlords just do not use it.

There Is a Better Way to Cover the Gap

Instead of bleeding after-tax income into the rental every month, you borrow the shortfall from a Home Equity Line of Credit (HELOC). Under paragraph 20(1)(c) of the Income Tax Act, interest on money borrowed to earn rental income is fully tax deductible. That one shift dramatically reduces your real after-tax cost compared to using cash from your paycheque. But the HELOC covering the shortfall is not a standalone move. It is one piece of a larger structure called cash damming, and that is where the real acceleration happens.

If you are in a 43% marginal tax bracket, every $500 you pull from your chequing account actually costs you closer to $875 in gross earnings. Borrowing the same amount from a HELOC at current rates costs you a fraction of that in interest — and that interest is deductible. The math is not even close.

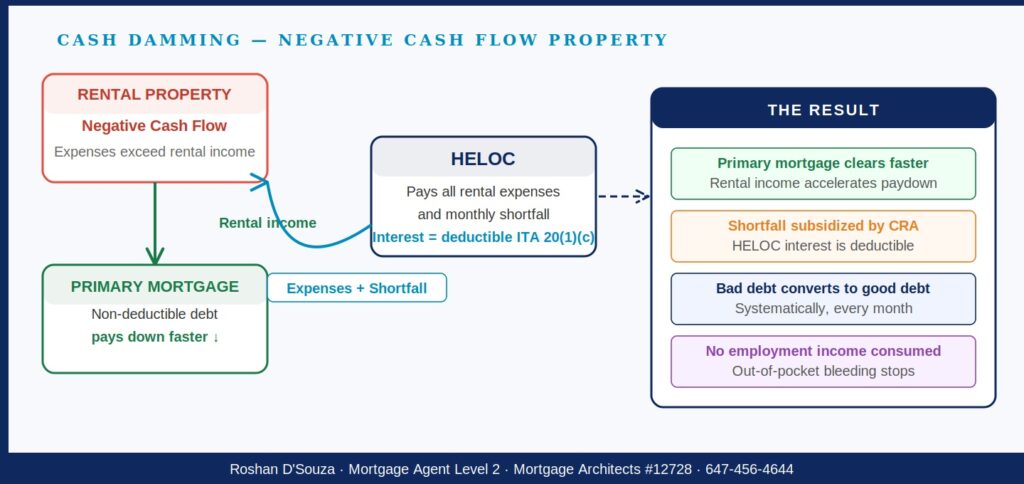

Then You Take It a Step Further: Cash Damming

The HELOC strategy is just the first layer. The deeper move is called cash damming, and it is one of the most underused tax structures in Canadian real estate.

Here is how it works. Your rental income, instead of going toward rental expenses, gets applied directly to your primary mortgage every month. Meanwhile, the HELOC covers every rental expense — the shortfall, property taxes, insurance, and maintenance.

As your rental income pays down the primary mortgage, the HELOC balance — used exclusively for deductible rental expenses — grows. CRA allows this recharacterization because the purpose of the borrowing is clearly income-producing. Every single month, your non-deductible personal mortgage shrinks faster, and your deductible investment debt grows in its place. You are not just saving on interest — you are systematically converting bad debt into good debt, on autopilot, without changing your lifestyle or cash flow.

Who This Works For

This structure works well whether you have one rental property or two. The setup typically takes a few weeks, but once it is running, the compounding builds for years.

There is one important prerequisite: this strategy requires a readvanceable mortgage — a product like Manulife One, Scotiabank STEP, TD FlexLine, or equivalent. These products allow your available HELOC credit to automatically increase as you pay down your mortgage, which is what makes the cash-damming mechanism work. Without a readvanceable product, the strategy does not function mechanically.

The landlords who benefit most are those who have equity in their primary home, a mortgage they can advance or obtain, and a rental running at a small monthly shortfall. If that sounds like you, the question is not whether this strategy works — it is how much it is already costing you to not use it.

The Long Game: Mortgage Freedom Faster

Most people think paying off a mortgage faster means making extra payments. Cash damming does something more powerful. It accelerates the paydown of your non-deductible mortgage automatically, every month, using money that was already flowing through your property.

Over a 25-year amortization, a landlord running cash damming from year one can shave years off their primary mortgage while simultaneously building a fully deductible investment debt structure. The result is not just tax savings. It is owning your home free and clear sooner, with a portfolio of deductible debt that works in your favour at tax time.

That is the real prize. Not just covering a shortfall cheaply, but turning a rental liability into a tool that buys back your financial freedom.

What To Do Next

If you are covering a rental property shortfall in Canada with after-tax dollars, book a 15-minute strategy call. I will map out whether this structure works for your specific numbers. No pitch, just math.

Or forward this to a landlord friend who is writing that cheque every month and has no idea the tax code would help cover it.

This post is for informational purposes only. Please consult a qualified tax professional before implementing any tax strategy.